The Medical Futurist | August 3, 2019

Why did activity trackers flood the digital health market, while there’s barely a company dealing with menopause, arthritis, or rare diseases? How do digital health investors decide when it comes to funding a new project, and what are the specific factors to take into account in relation to the healthcare market? We looked around what could scare off financiers from funding tough medical issues, and have a suggestion on how to bring forward solutions for marginalized health problems. Read on.

Investment in digital health for everyone?

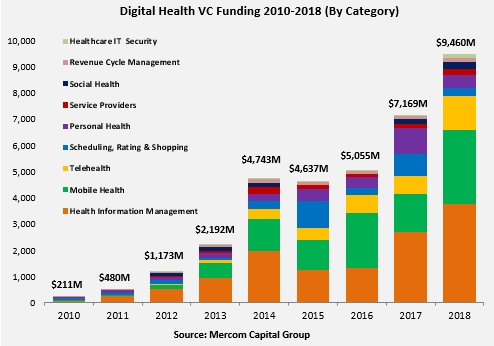

Investment in healthcare, especially in the digital health market, is growing steadily in the last years. In 2018, investment in digital health startups even hit a new high totaling $8.1 billion across 368 deals, although the market seems to be only slightly slowing down when looking at the first numbers from 2019. All in all, digital health companies raised a total of $4.2 billion in 180 deals during the six-month period, Rock Health found. This happens in spite of the fact that ninety percent of start-ups in the medical market will die or be ‘acqui-hired’ within 2 to 5 years from inception.

According to Mercom’s annual report, the highest funded categories in 2018 included data analytics with $2.1 billion, mHealth apps with $1.3 billion, telemedicine with $1.1 billion, mobile wireless technology companies with $847 million, clinical decision support with $714 million, and wearable sensors technology companies with $703 million. What we cannot see from these categories is the layers of financing and the issue areas that remain usually underfunded. For example, women’s health issues, such as menopause, endometriosis, period pain, or issues around mental health troubles, not to speak about the issues of remote communities in both developed and underdeveloped communities, or the universe of rare diseases.

So, we tried to figure out the reasons why venture capitalists, lenders, and other backers would not dip their toes into deeper waters just to tell them that healthcare is not (exclusively?) about profit-maximizing but to heal patients and create a better place for everyone out there. We are aware of the fact that we seem to be idealists and perhaps a bit naïve to think that digital health investors would consider factors other than crude numbers, that’s why we believe other stakeholders should step up as investors or at least co-financiers: non-profit organizations, incubators (perhaps initiated by large companies), and governments. Namely, actors whose interests don’t exclusively revolve around profits and are able to push issues that the market would otherwise leave out.

For example, the Bill & Melinda Gates Foundation offers grants for digital health solutions that address issues of importance in global health priority areas. Such initiatives could encourage solutions focused on particular issues of particular communities that would otherwise remain underfunded. But let’s see why exactly would they be denied investment?

What could scare off investors from financing tough healthcare topics?

1) Healthcare is not designed to be open to innovations

Healthcare is a difficult area: many stakeholders from payers through providers to the patient community, countless regulations, and the inner logic of the industry. Thus, it requires another mindset from investors trying to set their feet on the healthcare market.

To make it even more complicated, the healthcare industry has an aversion to major change. It is not easy to “disrupt” here anything as stakeholders are interested in maintaining the status quo. “In case of a lot of these large healthcare enterprises, payers, providers, there’s actually an incentive to do nothing because you may disrupt your existing business lines. … So when we look at potential investments in the health tech space, we’re looking for the kind of 10x improvement in the overall workflow that they’re touching”, said Dr. Dan Gebremedhin, a partner at the health venture capital, Flare Capital, at a recent conference in Philadelphia. That largely explains why digital health has proportionately more recurring investors than new ones, as well as the inclination to fund “tried and tested” issues – unless it promises to outperform standard industry practices by the mentioned at least ten times.

However, since the Theranos debacle, investors are generally more cautious with disruptors. They have learned from past mistakes and continue to rather fund startups with business-to-business models, a Rock Health report also said. Their researchers found that 87 percent of funded digital health companies in the first half of 2019 sell to enterprises such as employers, payers, providers, and others that hold the purse strings in U.S. healthcare.

2) The potential scale of the target market is too wide: everyone or just a tiny fracture

Beyond the healthcare universe in general, investors having increasing ROIs and constantly growing numbers in front of their eyes could have an inclination towards digital health solutions that promise to solve issues for everyone. Telemedical platforms could be useful for both children and the elderly, both men and women, both patients and physicians, while a clinically validated menstruation tracking app slices the potential target market in half. That’s the same reason when it comes to other health topics that only affect certain communities, minorities, or patients with rare diseases.

Moreover, we find similar issues when looking at language barriers: as developers reach higher population numbers with digital health solutions in English, there’s less thought (and funding) given to Spanish, French, or Swahili innovations.

3) The beast called accurate measurements

Developing health sensors, wearables, diagnostic devices, or any other gadgets that measure health parameters or vital signs requires tremendous efforts. However, there are certain parameters that are far easier to measure than others. For example, it is not a surprise that you cannot find an activity tracker, a smartwatch, or even a smartphone without the ability to count steps or measure pulse rate. However, it is far more difficult to figure out how to accurately give a reading for blood glucose, for ECG, or for blood pressure.

That’s why the digital health market started to move into the direction of fitness wearables and activity trackers, and innovations in the area of disease management or diagnostics have still a lot less to offer. Take the example of the Omron HeartGuide blood pressure monitoring smartwatch. The Japanese company’s achievement, meaning that they can measure blood pressure on the wrist is technically impressive, although it took them several years to develop the feature and months to go through the FDA’s approval procedure – and it still cannot offer the user-friendliness for all demographics that we would have expected.

4) Evidence-based medicine, clinical testing, and validation takes time

The technology market moves extremely fast: smaller and smaller smartphones, thinner and thinner flat-screen televisions come along every single day. As the digital health market is a combination of the technology and healthcare sectors, the speed of the technology market drives investors towards solutions that require the least amount of time possible to bring a solution to market.

However, healthcare doesn’t work like that. Evidence-based medicine requires time and energy. Medical technologies, drugs, or healthcare solutions need years to develop. It takes years to experiment with the right ingredients in the lab, to put together the most fitting design, or to create the most accurate measurement process. Afterward, the testing, as well as the market approval phase, begins.

Nevertheless, when looking at the digital health universe, we can experience the clash of interests, and more often than not investors will go for products and solutions that require less time to complete. The rush for disrupting the market was also a factor in why Elizabeth Holmes got to the top so quickly with the infamous Theranos blood-testing company. Well, we all know how that ended, though.

5) Unconscious bias?

The technological universe still doesn’t present itself as a diverse landscape. Just look at how distorted the participation of women in technology or investment is. Women make up just 13 percent of decision-makers in venture capital in the UK. Female founded companies get less than 1 percent of total UK venture capital, while male founded companies get 89 percent, according to a comprehensive article in the Financial Times. That is despite the fact that a third of entrepreneurs in the UK are female.

In the US, companies founded solely by women received just 2.3 percent of the total capital invested in venture-backed start-ups, according to the same article. The numbers are similar in the healthcare space, too, however, we noticed a trend of increasing participation in the digital health universe – both from the developer’s and the investor’s side – when it comes to women.

Yet, unconscious bias could play a role, particularly for those in the (health) tech space when it comes to a decision about investment. While there are successful female founders, the most notable tech founders were young men, so investors are perhaps unconsciously looking for people that fit that mold. And when women come forward with female health issues in a room full of male investors – their chances are unfortunately considerably less for investment.

Just take the example of NextGen Jane. The Oakland-based start-up promises to get insights into female reproductive health through blood squeezed out of the tampons that women send them and detect early biomarkers for endometriosis, cervical cancer or other conditions with the help of their Smart Tampon platform serving as a sentinel system. It was founded five years ago but promises to send out its first products next year, all the while struggling with funding issues.

While many could argue that female reproductive health, rare disease management, or arthritis are health problems concerning only a fraction of the population – and thus it is not worth investing large sums into it – we do believe that every life is worth saving, and every patient is worth healing, no matter how small that issue might seem. That’s why digital health investors might partner more with actors, such as non-profit organizations, governmental agencies, or foundations that not only have profits in their interests, in order to secure the necessary funding for developing digital health solutions for marginalized health problems. Everyone could benefit from that.